Like

many Americans, my mom has no retirement savings.

By

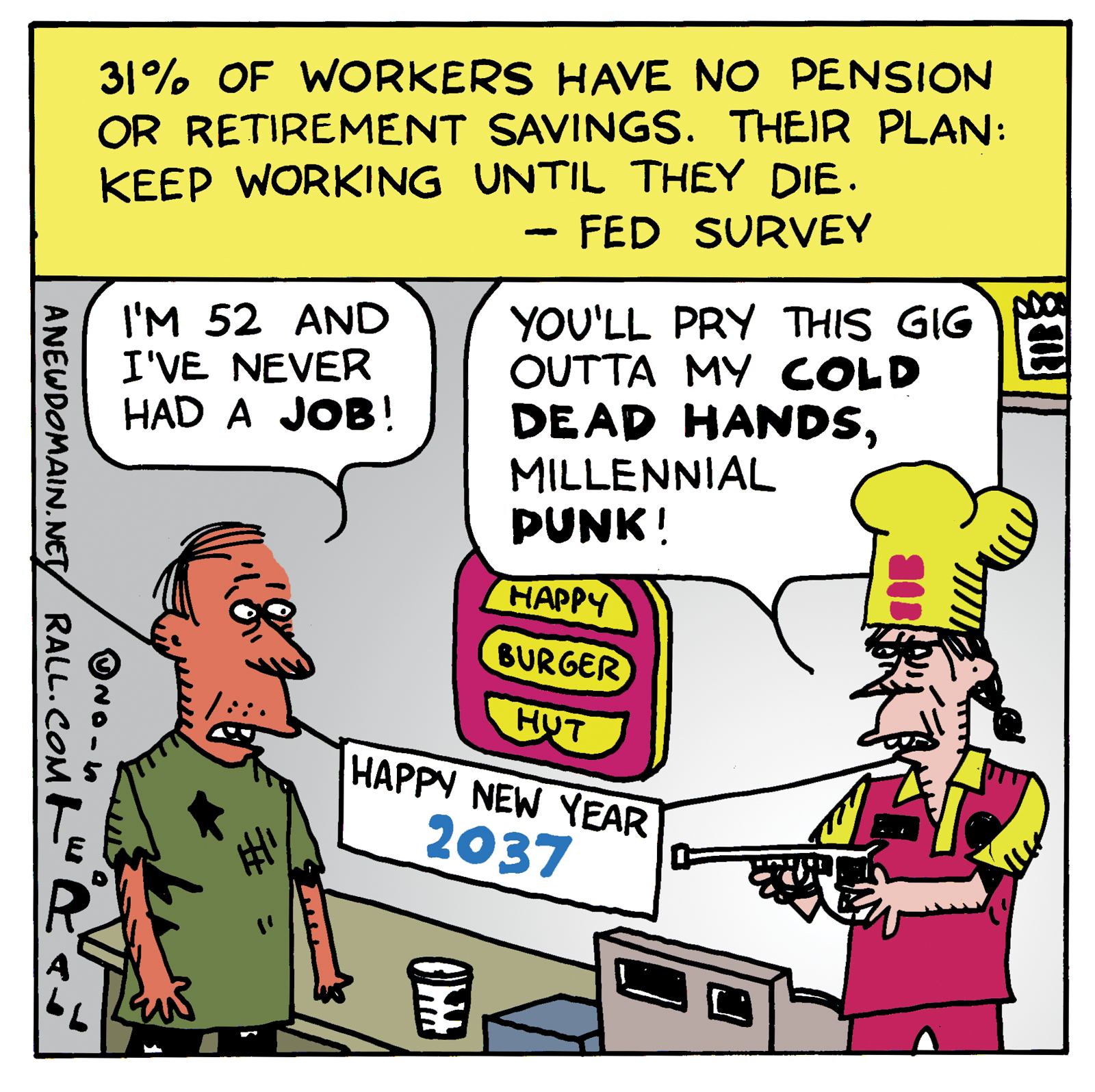

“My plan is just to work until I die.” That’s how my mom sums up

her retirement prospects.

She’s worked more than 40 hours a week as a legal secretary in

north Florida for as long as I can remember.

When my brother and I were kids,

we went to her office every Saturday and entertained ourselves by sliding

across the floor in fancy law firm chairs while our single mom worked overtime

in her cubicle.

She managed to get me into college on a scholarship, and my

brother got there on the GI Bill after a stint in the Army.

Yet the American

dream still hasn’t quite paid off for her. My mom’s one of the 62 percent of

Americans who lives paycheck to paycheck.

Even at age 60, she still doesn’t have paid sick leave or vacation time, and she

avoids the doctor because she can’t afford her $2,000 deductible.

Because she had no savings, my coworkers at the

Institute for Policy Studies took up a donation drive to cover her travel and

time off work.

My IPS colleagues recently released a report on the retirement gap between CEOs and workers. They found

that nearly half of working age Americans have no

access to retirement plans through their jobs. When I asked my mom about her

own retirement savings, I learned she had nothing at all.

That terrified me.

My mom isn’t bitter about it. She does the best she can with

what she has, and tries to stay healthy.

When I asked her permission to share

her story, she was worried that it might sound like she was complaining.

As for me, I felt angry.

The 100 CEOs profiled in this report have nest eggs that are

worth more than $49 million — enough to generate a $277,686 monthly retirement

check for the rest of their lives.

My mom’s anticipating a Social Security

check worth about $1,200 a month starting five years from now — and year after

year we hear politicians threaten to cut even that.

In fact, millions of Americans rely on the federal government’s

safety net to support them in retirement. But the net is fraying as

corporations and their top executives dodge their fair share of the taxes that

sustain it.

While they pad their own retirement accounts, people like my mom

who work hard their entire lives could have nothing to show for it.

What can be done?

My colleagues have suggested capping tax-deferred,

corporate-sponsored retirement accounts at $3 million, a move that President

Barack Obama estimated would raise an additional $9 billion of tax revenue over 10 years.

Funds

from an annual excise tax on assets greater than $3 million could go to the

Social Security Trust Fund, which would help all workers.

Even with that cap in place, the richest corporate retirees

would get $200,000 a year to live on in retirement. I bet they’d be able to

make do.

Here’s another good idea: Close the “performance pay” loophole

that allows unlimited corporate tax deductions for executive pay. The Joint

Committee on Taxation estimates that closing this loophole would generate more than $50 billion over 10 years.

My mom and other low-income and middle-class workers shouldn’t

have to go it alone. It’s time for all of us to stand together and demand

fairness in retirement. I don’t want her, or anyone else’s parents, to work

themselves into the grave.

Tiffany

Williams is the associate director of the Institute for Policy Studies. IPS-dc.org

Distributed by OtherWords.org.

Distributed by OtherWords.org.