Lower

the age for required withdrawals

By

Gerald E. Scorse, Progressive Charlestown guest columnist

|

| RMD is an alternate acronym for MRD |

On

the bright side, Furman said there was “increasing agreement that we can get

additional revenue while improving efficiency through broad-based reductions in

tax expenditures for those who derive outsized benefits…under the current

system.”

Putting

it more simply, those who reap the richest rewards should be first in line when

the tax reformer cometh. It’s a fairness argument, and Furman claimed it had

won the minds of former Council chairs Martin Feldstein, Glenn Hubbard and Greg

Mankiw.

Congress

should follow their lead and start with the fairest, kindest tax reform of all:

a stepped-up timetable for minimum required distributions (MRDs) from

tax-deferred retirement accounts. It would bring billions into the Treasury by

directly raising certain incomes; could reform be any kinder?

Recall

that Furman used the phrase “outsized benefits.” Tax-deferred retirement

accounts offer the same breaks to everybody: pre-tax contributions, untaxed

investment growth.

High-income

workers take more advantage, but that’s to be expected. The real outsizing

flows from minimum distributions.

To

learn how it happens, let’s look at the role of MRDs and the rules that govern

them.

Withdrawals

from tax-deferred accounts effectively pay the country back for more than 40

years of compound tax breaks. The payback is the income taxes that come due

when savers dip into their nest eggs.

There

are two options for withdrawals. One is for people who need the money, the

other for those who don’t.

The

first group gets penalty-free access as early as age 59 1/2. Each withdrawal

triggers a tax payback, and smaller balances limit potential gains going

forward.

Those

who don’t need the money can keep it invested (and likely growing) for another

11 years. Minimum required distributions don’t begin until age 70 1/2, and when

they do the accent falls heavily on minimum.

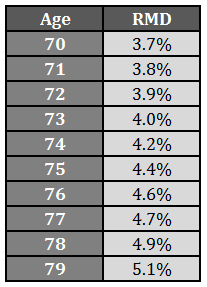

The

formula that applies to most accounts calls for a starting distribution of

under 3.7 percent. The percentage rises yearly, ever so slowly. Twenty-five years

later, at age 95, the MRD is just a shade over 11.6 percent.

MRDs

in fact double as MRTs: minimum required taxes. Ironically, the rules turn the

biggest beneficiaries of tax-deferred accounts into outsized laggards at paying

America back.

The starkest example is so-called stretch IRAs. They can

string out distributions for generations, even into the next century. President

Obama has long been trying to end them; a proposal in his 2016 budget would

require most second inheritors to close out their accounts within five years.

This change alone would raise an estimated $5.5 billion

over the next decade.

Far more important, though, is basic reform: MRDs should

begin at age 65. The qualifying year for Medicare is a fitting year to begin

repaying the Treasury for those decades of tax breaks (and, in the bargain,

helping to keep Medicare solvent). If the current withdrawal percentages made

the same five-year shift, the required distribution would reach 11.6 percent at

age 90 instead of 95.

In addition to fairness, there’s powerful fiscal reason

to create an accelerated MRD schedule for future retirees. Unlimited billions

would stream into the Treasury.

About 10,000 Americans turn 65 each day, a

demographic tide that’s set to roll in until 2030. This year also marks the

beginning of required distributions for the first of the country’s 78 million

baby boomers. (And no, higher minimums won’t exhaust their savings. Only

withdrawals well beyond the minimums could do that.)

Larger distributions would

also put more money into people’s hands; if the money gets spent, it would help

stimulate the economy and grow jobs.

Summing

up, minimum distributions should start sooner and grow a touch faster. When

Congress finally takes up tax reform, it should begin with the fairest and the

kindest.

Gerald E. Scorse

helped pass the bill requiring basis reporting for capital gains. He writes on

taxes.

©

2016 Gerald E. Scorse